Oh hi! I thought I would pause on writing about babies for a moment, and go back to my original baby and first love: money.

Ha! You think I'm kidding, but those close to me will attest... I have been a fan since a young age.

It has been 4 years since this post on how I view money, my do's and don'ts about what I will spend on, and so many big things have happened since.

Fundamentally, I would say that my relationship to it has not changed, but structurally, a lot has.

So! Let's indulge! Get it all out in the open!

I am endlessly fascinated and grateful when others talk openly about their pragmatic and philosophical approaches to money, so I am happy to update this space on what has changed in my world.

(Just like last time, if this topic bores you, I would skip this post.)

//

To refresh your memory, and to introduce the topic to those who are new to my writing:

When last we spoke about finances in 2014, I was

- about to turn 30 later that year

- had just gotten married

- had just moved to Vancouver from the Yukon

- really into spending on money on food

- really into typing lists

At that point, B and I had been together for about 5 years, and we had always kept our money separate. I believe we had one shared credit card, but each retained our own private cc as well. When the shared bill came each month, we subtracted our own expenses, and then split the remaining shared balance down the middle, 50/50. This was our set-up, that we were both quite happy with, well into our first year of marriage.

Here is what the last four years since have evolved into:

- WE MERGED OUR MONEY. I have to tell you, it was panic-inducing for both of us. I was a life-long miserly saver, and he was an anti-capitalist dude with a penchant for material things, so suffice to say that many, many frank conversations were had about what we envisioned our shared values to be.

- Within a few months, it was as if it had always been that way -- and, at least for me, I stopped viewing it as "my" money begrudgingly lumped in with his. Nowadays, I always think "ours" and it feels healthy, and happy, and safe.

- We named me CFO (Chief Financial Officer) of the family. I get kind of power hungry sometimes.

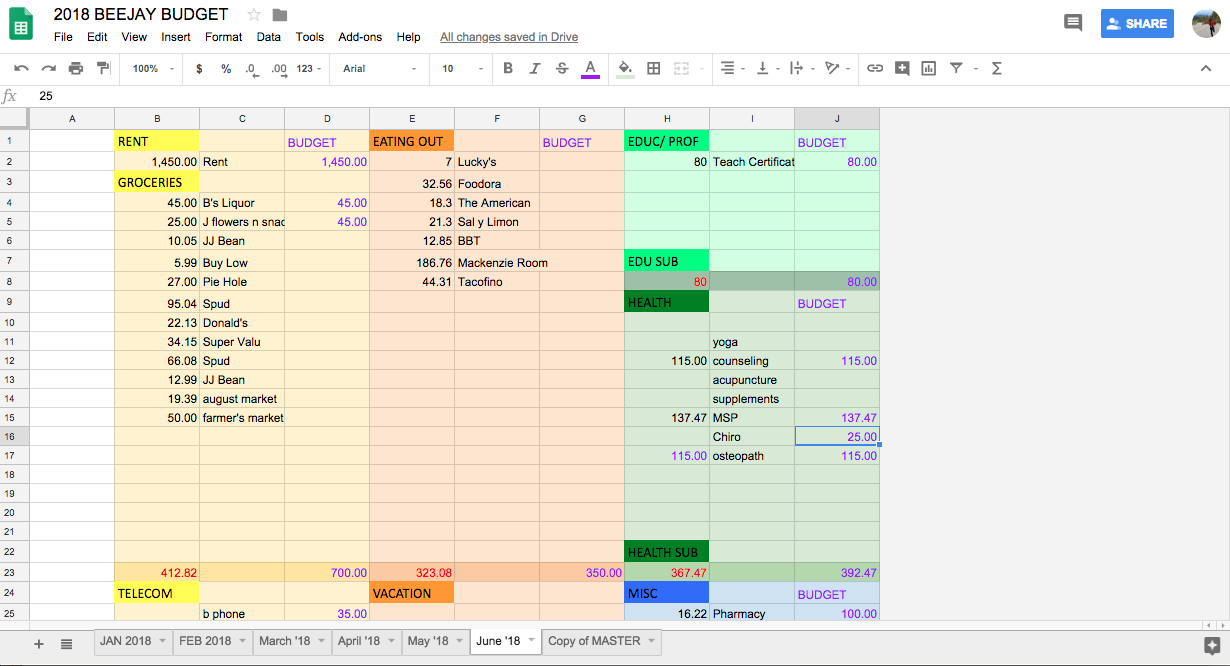

- We started to track ALL purchases, down to bus fare and the cost of a single doughnut, and learned a ton about our family spending habits. I have a sexy Excel spreadsheet that I update every month.

- Sexy Spreadsheet (SS) is comprised of the following categories:

- Survive (rent, groceries, phone bill, transportation)

- Thrive (eating out, vacation, recurring donation, streaming services)

- Health (chiro, counselling, MSP, etc.)

- Miscellaneous

- Survive budget numbers stay relatively the same month to month. By now, I know we spend $700 on groceries a month, if not a bit more. I had to wrestle with that number for a long time in disbelief. But we choose to buy organic, and use SPUD, and lots of fresh stuff so... it is what it is. Thrive budget numbers change a bit more, particularly for eating out. If it's a birthday month or a busy month, I increase the eating out budget from $250 to whatever is reasonable.

- Yes, we spend a lot of money on food.

- Oops, I should have said first and foremost that we save 30% of our income before accounting for expenses. This percentage is fairly arbitrary, and in lean years has been less -- and in plentiful months has been adjusted for more. This is the average.

- In this past year, I implemented a new system where this savings is further subdivided in SS into its own categories. I was finding that just saving a lump sum was not maximizing its potential-- it kind of just sat there accumulating as a Rainy Day fund, but once we reached our target goal for emergency purposes (3-6 months worth of income), it kind of lay around in a heap. Meanwhile, we felt unsure or guilty about big, fun purchases -- like can this come out of that fund? Or should it grow to infinity?

- So the categories for savings in SS rotates all the time. Currently, it includes:

- Future Unemployment (for our summer months as teachers, maternity leave, and other dips in our career. *Fun fact, teachers do not get paid over the summer. If you know someone who does, it is because they have elected to have their annual salary paid out to them over 12 months, instead of 10. I bring this up because it irks me when people have said to me that we are lucky to have paid summers off. NO. *)

- Retirement / Investment (the latter being real estate, hahahaahahahahahahah *crying*)

- Car Kitty

- TV fund (did you know in the almost 10 years we've been together, we've used a laptop to watch all our shows? Did you know that we love watching our shows? So silly.)

- Aloha / Yukon/ Lummi (upcoming vacations)

- RESP (for baby)

- Each of these categories get their own accounts in our Coast Capital online banking. Each month we decide how much of our savings should go into each pot. For example, if we are saving $1000 that month, I might put $300 towards Retirement, $300 towards Future Unemployment, $50 towards Car Kitty, etc.

- It is the highlight of my month when I get to transfer these sums into their accounts. I am not being hyperbolic. It is like watching my children grow.

- I think it goes without saying, but because of all these safeguards, we do not spend beyond our means. This summer when we are down to just my maternity EI as income, we will dip into our Future Unemployment account which was created for circumstances like this. Then, the rest of the year we start filling it back up again.

- After savings and expenses have been accounted for, the remainder is FUN FUNDS! This number is divided evenly between the two of us, and that is what each partner gets to play around with, no judgement. A monthly allowance.

- My fun funds: I am very willy nilly with this. I don't budget myself or keep track very much. Some months I spend more than what I receive. It has always evened out.

- What I Spend on: when I re-read my 2014 post, I realized my values have not changed in regards to this very much. I still do not buy fast fashion, and have taken it up a notch in that I try to splurge on ethically made items where I have confidence that workers are treated well and compensated adequately. I buy far less, but pay more. Other things: food. That's it. I'm simple.

- Simple to the point that I was saving way more than B because his interests and hobbies are more expensive (snowboarding, tattoos, alcohol), so last year I spontaneously flew to Los Angeles with my schoolwife, in an attempt to even out our fun funds (and to celebrate the completion of my Masters).

- We were able to pay for my Masters, as predicted in 2014, without taking out a student loan! Yay!

- Oh, I do go insane at the Farmer's market though. Insane. I don't even count when I'm there. Listen, I tried taking up a bread making hobby and I understand now why handmade loaves of sourdough bread are like $200.

- We stopped putting our investment money into GICs, and have been putting it into our TFSAs. I basically choose medium risk mutual fund type things, and blindly put what we can afford into those. I say blindly because I still feel like I'm pretending to be a grown up when I use 'investment' in a sentence. This is one area I would like to feel more adept at.

- Since 2014, I got over my fear of spending money on furniture and now it's like: bring me all the teak and brass and indigo.

- Flowers finally made it into the joint budget last month!

- Re: baby. Aside from preliminary expenses, baby has not impacted our bank accounts very much. This will change as he gets older and I go back to work full time, but he is still very small and my booby still makes very free food. We are grateful to live in Canada and receive maternity EI and monthly Universal Child benefits.

I think that is it. If you made it this far, you a) share a healthy interest in finances like I do, or b) you are a bit nosy like we all are, and perked up when you knew I was disclosing some things that are usually kept taboo in society. Either option is awesome! We could all stand to be a bit more candid about this topic.

What is on my / our horizons in terms of $$$...

- changing our minds daily about whether to invest in property or rent forever or move somewhere where a dilapidated house does not cost $1.4 million dollars

- learn more or take some educated risks with our investments

- should we get life insurance?

- this reminds me, Oh god we need to create a will, husband.

I was reading today that it might be helpful (especially if you are the don't-like thinking-about-money type) to frame it in terms of: what are my values regarding what my money can provide me? For us, it would be: security, adventure, pleasure, generosity / charity.

How about you? Any pragmatic or abstract goals you have for your $ this year? If you're part of a couple, how do you navigate sharing finances?

Impressive! A short masterclass in money management. Too bad it isn't a high-school required class ...one term anyway . Hugs,karen

ReplyDeleteAs I think you know, I also love money talks. I love saving and splurging on certain things once I have saved. It’s only in the last five years that I’ve relaxed about ordering what I want on a menu instead of what’s the cheapest (I travelled through Italy eating only pizza margarita). And my husband is also an anti-capitalist who in his heart hurts/angers that we have money when others do not...but also loves bikestatooscocktailsdeliciousfood. So, finding the shared values is a continual conversation. Having a baby highlighted some is the commonalities for us: Henry’s education is a priority, security for the unexpected, and things that bring joy (travel, books, clothes that cost too much and all of the food). We’ve been reflecting lately on a constant feeling of pressure to make a bit more, spend a bit less, have a bit more, own a bit more. And I’ve been thinking about housing in this vancouver market and how if two university educated professionals are feeling a crunch, there is a whole additional population with even less housing security. Especially families. Not sure where I fit into that, but it’s been on my mind with regards to distribution of wealth and access to resources. Thanks for sharing! Hopefully see you soon!

ReplyDelete